Thoughtful perspectives on liVING, career decisions, and wealth building.

Financial Planning for Doctors: From Medical School Loans to Long-Term Wealth

Learn financial planning for doctors from medical school loans to long-term wealth creation. Discover how MBBS and MD doctors can manage education loans, invest salary smartly, plan retirement, and build wealth across government and private practice careers.

FINANCE FOR WORKING PROFESSIONALS

2/18/20265 min read

Doctors invest nearly a decade building their careers before their income stabilizes. By the time earnings begin, many carry education loans, delayed savings, and family responsibilities. Financial planning for doctors must account for delayed income, high stress, uneven earning curves, and strong long-term potential.

This guide walks through the financial journey of doctors—from MBBS to senior consultant—covering loans, government vs private practice income, and a clear, age-wise investment strategy.

1) Medical Student Phase (Age 18–24): Awareness Before Income

Costs are high, income is zero. Focus on:

Choosing structured education loans over informal borrowing

Avoiding lifestyle debt

Learning basics of budgeting, insurance, and investing

Building a clean credit history

Goal: financial literacy and damage control—not investing yet.

2) Early Career (Age 25–30): Internship & Junior Residency

Income begins but remains modest. This phase sets habits.

Monthly Income Allocation (guideline):

Living costs: 55–60%

Education loan repayment: 25–30%

Investments: 10–15%

Investment Split (of the 10–15% invested):

SIPs (equity mutual funds/index funds): 60%

FDs / liquid funds (emergency buffer): 25%

Precious metals (gold ETF/SGB): 10%

Direct stocks (optional, learning allocation): 5%

Focus:

Build 6 months’ emergency fund

Start small SIPs for habit formation

Health + term insurance

3) Degree Path Impact: MBBS vs MD/MS

MBBS-only doctors typically see steadier but slower income growth.

MD/MS or super-specialists face higher loans but higher earning ceilings.

MBBS Track (Age 28–35) – Monthly Allocation:

Living costs: 50–55%

Loan repayment (if any): 20–25%

Investments: 20–25%

MD/MS Track (Age 28–35) – Monthly Allocation:

Living costs: 45–50%

Loan repayment: 25–30%

Investments: 20–25%

Investment Split (of invested portion):

SIPs (equity funds): 65–70%

FDs/liquid funds: 10–15%

Precious metals: 5–10%

Direct stocks: 5–10%

International equity (optional): 0–5%

Focus: aggressive loan reduction alongside disciplined investing.

4) Workplace Reality: Government vs Private Hospitals

Government Hospitals

Pros: stability, predictable increments, retirement benefits

Cons: slower salary growth

Private Hospitals/Nursing HomesPros: faster income growth, incentives

Cons: variability, contract risk

Allocation Difference:

Government doctors can run consistent SIPs and long-term plans with lower buffers.

Private doctors should keep a 12-month emergency fund and avoid lifestyle inflation.

5) Prime Growth Phase (Age 30–40): The Compounding Decade

Income rises significantly. This is the most powerful decade for wealth building.

Monthly Income Allocation:

Living costs: 40–45%

Loan repayment (if any): 10–15%

Investments: 40–45%

Investment Split (of invested portion):

SIPs (equity mutual funds/index + flexi-cap): 55–60%

Direct stocks (selective, long-term): 10–15%

International equity funds: 5–10%

FDs/liquid funds: 10%

Precious metals: 5–10%

REITs/InvITs (real estate exposure without ownership): 0–5%

Optional Entrepreneurial Track (if clinic/nursing home is a goal):

Allocate 5–10% of income to a business fund (separate account)

Build capital for equipment, compliance, and working capital

Avoid using core retirement investments for business risk

6) Peak Earnings (Age 40–50): Scale, Then Stabilize

This phase brings peak income and higher responsibilities.

Monthly Income Allocation:

Living costs: 35–40%

Investments: 45–50%

Business/Real estate (optional): 10–15%

Investment Split (of invested portion):

Equity SIPs: 45–50%

Debt funds/FDs: 20–25%

Direct stocks: 10%

Precious metals: 5–10%

Real estate/REITs: 5–10%

Clinic/Nursing Home Ownership (if pursued):

Cap exposure to ≤25–30% of total net worth

Maintain separate personal emergency and retirement portfolios

Insure professional and business risks

Focus: build passive income, rebalance annually, protect capital.

7) Consolidation (Age 50+): Protect, Generate Income

Monthly Income Allocation:

Living costs: 45–50%

Investments/savings: 25–30%

Passive income assets: 20–25%

Portfolio Tilt:

Equity: 30–40%

Debt (FDs, high-quality bonds): 40–50%

Precious metals: 5–10%

Real estate/REITs: 5–10%

Focus: income stability, healthcare planning, estate planning, will.

8) Education Loan Strategy for Doctors

Prioritize higher-interest loans first

Use bonuses/incentives to reduce principal

Begin parallel investing once EMI is comfortable

Avoid extending loan tenure just to fund lifestyle upgrades

9) Insurance & Risk Management (Often Ignored)

Term life insurance (10–15× annual expenses)

Comprehensive health insurance beyond employer cover

Professional indemnity insurance

Disability insurance (if available)

10) Common Mistakes to Avoid

Delaying investing until late 30s

Lifestyle inflation after specialization

Overconcentration in clinic real estate

Trading frequently due to lack of time

Ignoring retirement corpus planning

11) Simple Rules Doctors Can Follow

Automate SIPs right after salary credit

Review annually; don’t micromanage markets

Increase investments with income hikes, not expenses

Keep business capital separate from retirement money

Rebalance asset allocation every 2–3 years

FAQs

1) When should doctors start investing if they have large education loans?

Start small alongside EMI once income stabilizes. Clear high-interest debt aggressively, but don’t delay habit formation.

2) How much should a young doctor invest monthly?

Aim for 10–15% early, rising to 30–45% as income grows in your 30s.

3) Are direct stocks necessary?

Not necessary. SIPs in diversified equity funds are sufficient for most doctors with limited time.

4) Should doctors buy real estate or open a clinic?

Only if financially prepared. Cap business exposure and protect retirement funds from business risk.

5) How often should portfolios be reviewed?

Once a year is enough. Avoid reacting to short-term market noise.

Final Thoughts

Doctors sacrifice early years to build a career of service. Financial planning ensures that sacrifice converts into long-term security. The winning formula is simple: disciplined saving, diversified investing, controlled lifestyle growth, and risk protection. Start early, scale smartly in your 30s and 40s, and protect capital as you approach consolidation years.

If you’d like, I can provide a printable age-wise allocation table, a retirement corpus calculator, or a one-page checklist for doctors to implement this plan.

Bonus Publications

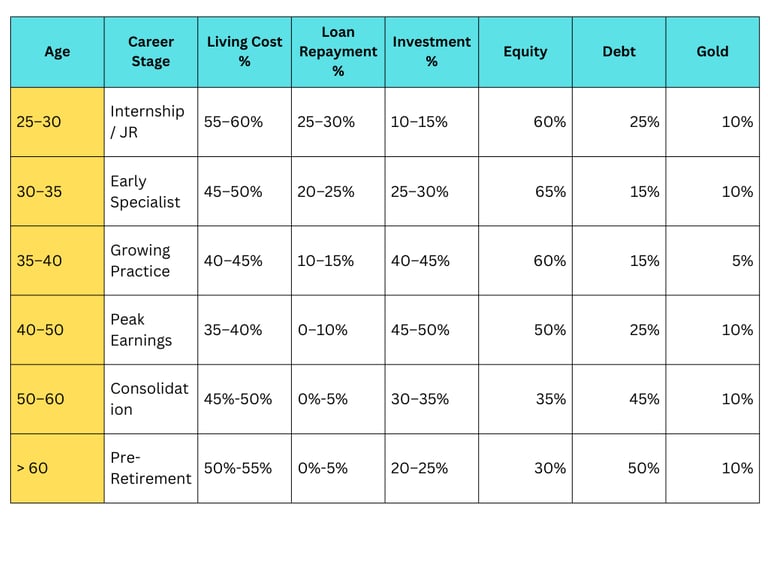

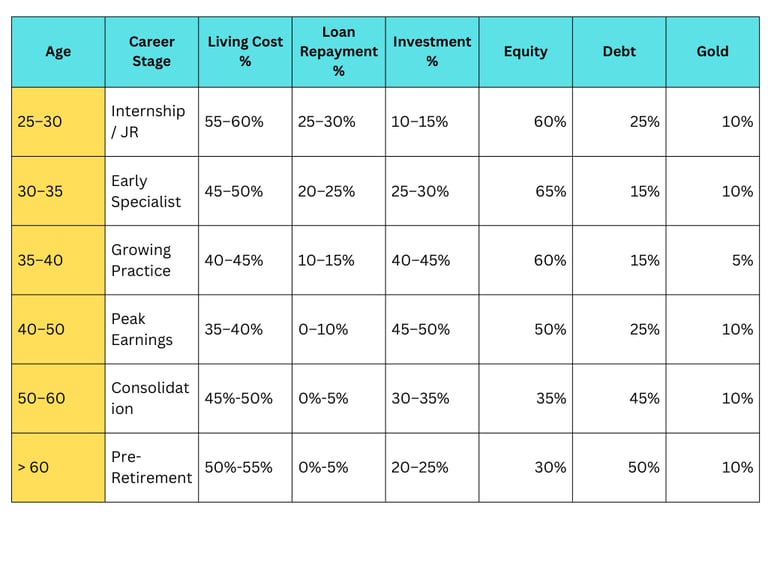

✅ Age-Wise Allocation Table for Doctors

Notes:

Equity = SIPs, index funds, diversified funds, selective stocks

Debt = FD, bonds, debt funds

Real estate/clinic allocation must not exceed 30% of total net worth

Increase investment % with every salary increment

✅ Retirement Corpus Calculator for Doctors

Now let’s calculate how much a doctor actually needs.

Step 1: Estimate Annual Expenses at Retirement

Example:

Current monthly expense: ₹1,00,000

Annual expense: ₹12,00,000

Assume inflation: 6%

Years to retirement: 25

Future Expense Formula:

Future Expense = Current Expense × (1 + Inflation)^Years

Example:

₹12,00,000 × (1.06)^25

= ₹12,00,000 × 4.29

= ₹51,48,000 per year

So at retirement, doctor needs ~₹51 lakh per year.

Step 2: Retirement Corpus Needed

Safe withdrawal rate assumption: 3.5%–4%

Corpus Needed Formula:

Corpus = Annual Expense ÷ Withdrawal Rate

Using 4% rule:

₹51,48,000 ÷ 0.04

= ₹12.87 Crores

So retirement corpus required ≈ ₹13 Crores

✅ Simplified Retirement Corpus Shortcut Rule

You can also use:

Required Corpus = 25 × Annual Expenses at Retirement

If retirement expense = ₹50 lakh

Corpus needed = ₹12.5 Crores

✅ How Much Should Doctors Invest Monthly to Reach ₹13 Crores?

Let’s assume:

Current Age: 35

Retirement Age: 60

Years to invest: 25

Expected return: 11% (equity heavy portfolio)

Using SIP calculation approximation:

To reach ₹13 Crores in 25 years at 11% return:

Monthly SIP required ≈ ₹1.2 – ₹1.4 lakh

If doctor starts at age 40 instead of 35:

Required SIP jumps to ≈ ₹2.3 – ₹2.6 lakh

This shows one critical truth:

Delay by 5 years = double the effort required.

✅ Practical Retirement Strategy for Doctors

Age 25–35:

Build habit, not corpus

Focus on loan clearance + early SIP

Age 35–45:

Aggressively increase SIP by 10–15% every year

Direct bonuses into investment

Age 45–55:

Shift gradually from 70% equity → 50% equity

Protect corpus

Age 55+:

Focus on income generating assets

Create laddered FD + bond structure

✅ Key Financial Planning Truth for Doctors

Because income starts late, doctors must:

Increase savings rate faster than peers

Avoid luxury lifestyle upgrades too early

Invest aggressively in 30s and 40s

Protect against professional burnout

Separate clinic investment from retirement fund

Connect

Questions? Reach out anytime, we're here.

lifeworkwealth@gmail.com

© 2026 Life Work Wealth.

All rights reserved.All content published on this website is for informational and educational purposes only. No part of this website may be reproduced, distributed, or transmitted in any form or by any means without prior written permission, except where permitted by law.